How to Start a Pension in the Face of Economic Armaggedon

-

Finally got around to making Junior S&S ISAs for the cubs. Should have done it earlier really but still gonna be looking at over a decade of investment for each, minimum.

Completely fucked my No Guilt Spending account which I felt too guilty to spend. -

Plans have hit a wee snag. My wife can't work for health reasons so gets UC. Once we have £16,000 in savings, she loses UC altogether. So I can't actually do too well with my ISA.

The good news is that money in a SIPP appears to not be counted so I'll need to concentrate more on that than the tracker/ISA stuff. -

Nothing wrong with a SIPP. You can still use a tracker fund within it."Plus he wore shorts like a total cunt" - Bob

-

Yeah seems to be essentially the same thing but just locked away. Which isn't an issue anyway.

-

The Mrs has a Stocks and Shares ISA with Halifax. Was just looking at fees and they charge £36 per year + £9.50 per fund trade. Which I think means if she switches fund it might mean 2 x £9.50 (sell trade + buy trade).

The Mrs has a Stocks and Shares ISA with Halifax. Was just looking at fees and they charge £36 per year + £9.50 per fund trade. Which I think means if she switches fund it might mean 2 x £9.50 (sell trade + buy trade).

Is this expensive? Should I be looking to shift her onto another platform? -

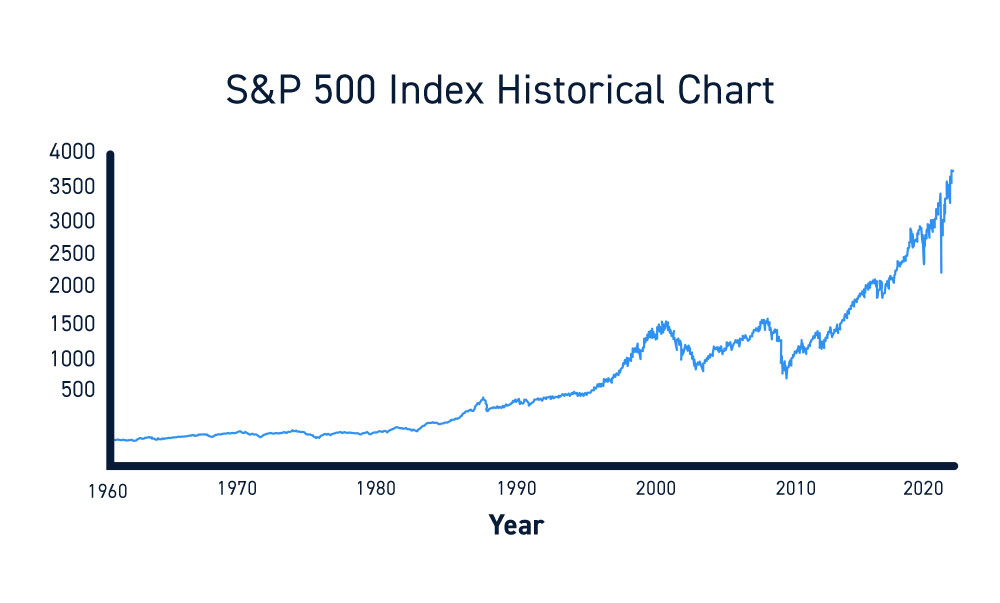

Spotted a Sunday Times Article claiming there could be a 10% to 30% drop on the 500 S&P in 2024. Couldn't read the article as it was gated but then heard on News Agents that it's come from a RW attempt to paint Biden as shit on the economy prior to the election, despite all the facts pointing to the opposite.

Spotted a Sunday Times Article claiming there could be a 10% to 30% drop on the 500 S&P in 2024. Couldn't read the article as it was gated but then heard on News Agents that it's come from a RW attempt to paint Biden as shit on the economy prior to the election, despite all the facts pointing to the opposite. -

"When everyone sells, I buy."I am a FREE. I am not MAN. A NUMBER.

"When everyone sells, I buy."I am a FREE. I am not MAN. A NUMBER. -

Show networks

Show networks- Xbox

- The Boy Roberts

- PSN

- TheBoyRoberts

- Steam

- TheBoyRoberts

- Wii

- BoyRoberts

Send messageb0r1s wrote:Spotted a Sunday Times Article claiming there could be a 10% to 30% drop on the 500 S&P in 2024. Couldn't read the article as it was gated but then heard on News Agents that it's come from a RW attempt to paint Biden as shit on the economy prior to the election, despite all the facts pointing to the opposite.

I've been thinking about a drop on the S&P 500. I know folks say you shouldn't try to "game" the system. But I'm seriously thinking about cashing out my SIPP soon and letting it sit as cash (perhaps as in some form of savings account if Hargreaves and Landsdown offers one) for a bit.

Really not sure what to do. -

30% is more than the financial crash and covid isn't it? Can't see what would cause that. Plus, it'll almost certainly recover, as it has done after those two incidents.

30% is more than the financial crash and covid isn't it? Can't see what would cause that. Plus, it'll almost certainly recover, as it has done after those two incidents. -

As per SG’s advice at the start of the thread - if the S&P500 crashes low, then it’s time to invest anything extra you can afford. Buy in while it’s cheap because we’re playing the long game.

As per SG’s advice at the start of the thread - if the S&P500 crashes low, then it’s time to invest anything extra you can afford. Buy in while it’s cheap because we’re playing the long game. -

To echo Goobs. 30% drop in <12 months of S&P500 is end of world stuff. Could happen! But erm pretty unlilkely in that timescale

-

The doom mongering has ramped up in the media this year I have noticed.

Must be an election year.

Don't worry, we'll all be conscripted soon.

edit: and Im deliberately paying less attention, the doom is still seeping in. -

Predict-o-matic: Trump wins the US election. Within a year announces alliance with Putin. Russia starts expansionist mini-wars all over the place, supported by US funds and infrastructure, beginning with anyone who provided aid to Ukraine. Like us.

S&P500 goes up thanks to all those sweet, sweet defence contract dollars. -

TheBoyRoberts wrote:

I've been thinking about a drop on the S&P 500. I know folks say you shouldn't try to "game" the system. But I'm seriously thinking about cashing out my SIPP soon and letting it sit as cash (perhaps as in some form of savings account if Hargreaves and Landsdown offers one) for a bit. Really not sure what to do.b0r1s wrote:Spotted a Sunday Times Article claiming there could be a 10% to 30% drop on the 500 S&P in 2024. Couldn't read the article as it was gated but then heard on News Agents that it's come from a RW attempt to paint Biden as shit on the economy prior to the election, despite all the facts pointing to the opposite.

I wouldn't do that with a pension. If it does drop, it should recover and you will recoup losses, plus if you continue paying in to take advantage of any dips, you still benefit from the drop.

However, if you were to cash out now and hope for a drop, it might not happen and you might end up buying in at a higher price. It might end up being a stellar play too of course, but ultimately it's more of a gamble. -

TheBoyRoberts wrote:

I've been thinking about a drop on the S&P 500. I know folks say you shouldn't try to "game" the system. But I'm seriously thinking about cashing out my SIPP soon and letting it sit as cash (perhaps as in some form of savings account if Hargreaves and Landsdown offers one) for a bit. Really not sure what to do.b0r1s wrote:Spotted a Sunday Times Article claiming there could be a 10% to 30% drop on the 500 S&P in 2024. Couldn't read the article as it was gated but then heard on News Agents that it's come from a RW attempt to paint Biden as shit on the economy prior to the election, despite all the facts pointing to the opposite.

If you're not sure what to do then do nothing. Even if you're sure what to do, unless it involves doing nothing, then do nothing. We should embrace the falls more than the gains.

OR, you could take one for the team and carry out your plan. When it next reaches an all time high we can all compare and see why it was a bad idea. This will be because invariably, you sold or bought back in too late, so you missed the big opportunity to stay in and buy monthly during any correction. This is how you make the most money, as illustrated by this graph:

Panicking will fuck the whole thing up. It'll take a nice juicy crash for everyone - once it bounces back, to see how that was the part that they made a wad. If it steadily just increases with no major drops we will not do as well. Preferably we want a crash to last a couple of years or so. Worry about crashes when your retirement comes up."Plus he wore shorts like a total cunt" - Bob -

Just to make sure everyone is getting the point, here's the vid again in the OP.

And another about why pricing is not investing.

In our case with an S&P 500, the business is the best 500 businesses. Buffet is rich because he's so old and he stays in the game. That's investing."Plus he wore shorts like a total cunt" - Bob -

I love how Buffet cuts through the drama. Wise words.

drumbeg wrote:The Mrs has a Stocks and Shares ISA with Halifax. Was just looking at fees and they charge £36 per year + £9.50 per fund trade. Which I think means if she switches fund it might mean 2 x £9.50 (sell trade + buy trade). Is this expensive? Should I be looking to shift her onto another platform?

In case you missed it Space Gazelle. Any tips on platform? Am I paying too much. -

Show networks

- Xbox

- The Boy Roberts

- PSN

- TheBoyRoberts

- Steam

- TheBoyRoberts

- Wii

- BoyRoberts

Send messageAll fair points!!

I’ll be staying put!!

Really do need to shout out to you all on this thread and say thanks.

Moving my old work pension into a sipp has (so far!) been one of the best financial decisions I’ve ever made.

Wouldn’t have done it if I’d not dipped in here.

Thanks!!! -

@drumbeg

Depends on how much you have in the fund. Shop about, but people here should not be concerned about fund trading fees. Just get the cheapest platform and the cheapest S&P tracker that they do. It's worth an annual look at platform fees to see if it's worth switching - go with the cheapest unless the cost of changing costs more, which it really shouldn't. It depends on circumstance.

https://www.moneysavingexpert.com/savings/stocks-shares-isas/"Plus he wore shorts like a total cunt" - Bob -

TheBoyRoberts wrote:All fair points!! I’ll be staying put!! Really do need to shout out to you all on this thread and say thanks. Moving my old work pension into a sipp has (so far!) been one of the best financial decisions I’ve ever made. Wouldn’t have done it if I’d not dipped in here. Thanks!!!

It's important you really understand why trying to time the markets is so bad. When you get that you can relax a bit. Some people just aren't suited to doing this and they're the people who sell when the markets are crashing. The long term game is all about the monthly investments and not doing anything. Preferably, do a direct debit once a month and never look at it. Try not to even think about it!"Plus he wore shorts like a total cunt" - Bob -

(or as a salary deduction, if you can)

(or as a salary deduction, if you can) -

Yeah, bonus points for that."Plus he wore shorts like a total cunt" - Bob

-

Show networks

- Xbox

- The Boy Roberts

- PSN

- TheBoyRoberts

- Steam

- TheBoyRoberts

- Wii

- BoyRoberts

Send messageSpaceGazelle wrote:

It's important you really understand why trying to time the markets is so bad. When you get that you can relax a bit. Some people just aren't suited to doing this and they're the people who sell when the markets are crashing. The long term game is all about the monthly investments and not doing anything. Preferably, do a direct debit once a month and never look at it. Try not to even think about it!TheBoyRoberts wrote:All fair points!! I’ll be staying put!! Really do need to shout out to you all on this thread and say thanks. Moving my old work pension into a sipp has (so far!) been one of the best financial decisions I’ve ever made. Wouldn’t have done it if I’d not dipped in here. Thanks!!!

I've done a lot of reading since posting and I couldn't agree more on trying to time the market now. The SIPP and my ISA will be staying as is.

As for the monthly investments advice; all being followed. I've got a fantastic current work pension (Civil Service Alpha pension) which just looks after itself. I've got a regular payment going into my ISA (S&P500 Acm) and a Environmentally friendly ISA.

I would love to be sticking money into my SIP, but at the moment, I feel a little exposed by a lack of readily available "normal savings", so I'm concentrating on getting those reserves built up before I start to stick regular payments into the SIP. -

Excellent. Just remember that you should explain to any partner why it's vital to keep putting into the tracker when the inevitable slump happens. We're taking advantage of all the people panicking and selling. When they sell it lowers the price for us and when they buy back it bumps it up. It's a win win. And don't forget the dividends, which aren't reflected in the S&P graph. As shareholders in all the companies we get a share of the profits too.

It's important that any partner understands this as it takes a bit of nerve to keep putting in during a spectacular crash and we will get one someday. When this happens just refer to this thread, where I'll be telling everyone to put even more in if they can afford it. That won't stop a partner thinking you're absolutely deranged so warn them in advance that the bad times are actually the good times."Plus he wore shorts like a total cunt" - Bob -

SpaceGazelle wrote:@drumbeg Depends on how much you have in the fund. Shop about, but people here should not be concerned about fund trading fees. Just get the cheapest platform and the cheapest S&P tracker that they do. It's worth an annual look at platform fees to see if it's worth switching - go with the cheapest unless the cost of changing costs more, which it really shouldn't. It depends on circumstance. https://www.moneysavingexpert.com/savings/stocks-shares-isas/

I'm thinking Vanguard. Fee free and they have an S & P fund. -

Just FYI, Vanguard have minimum inputs of £500 as a one off, or £100 monthly DD.

Howdy, Stranger!

It looks like you're new here. If you want to get involved, click one of these buttons!

Categories

- All Discussions2,715

- Games1,879

- Off topic836